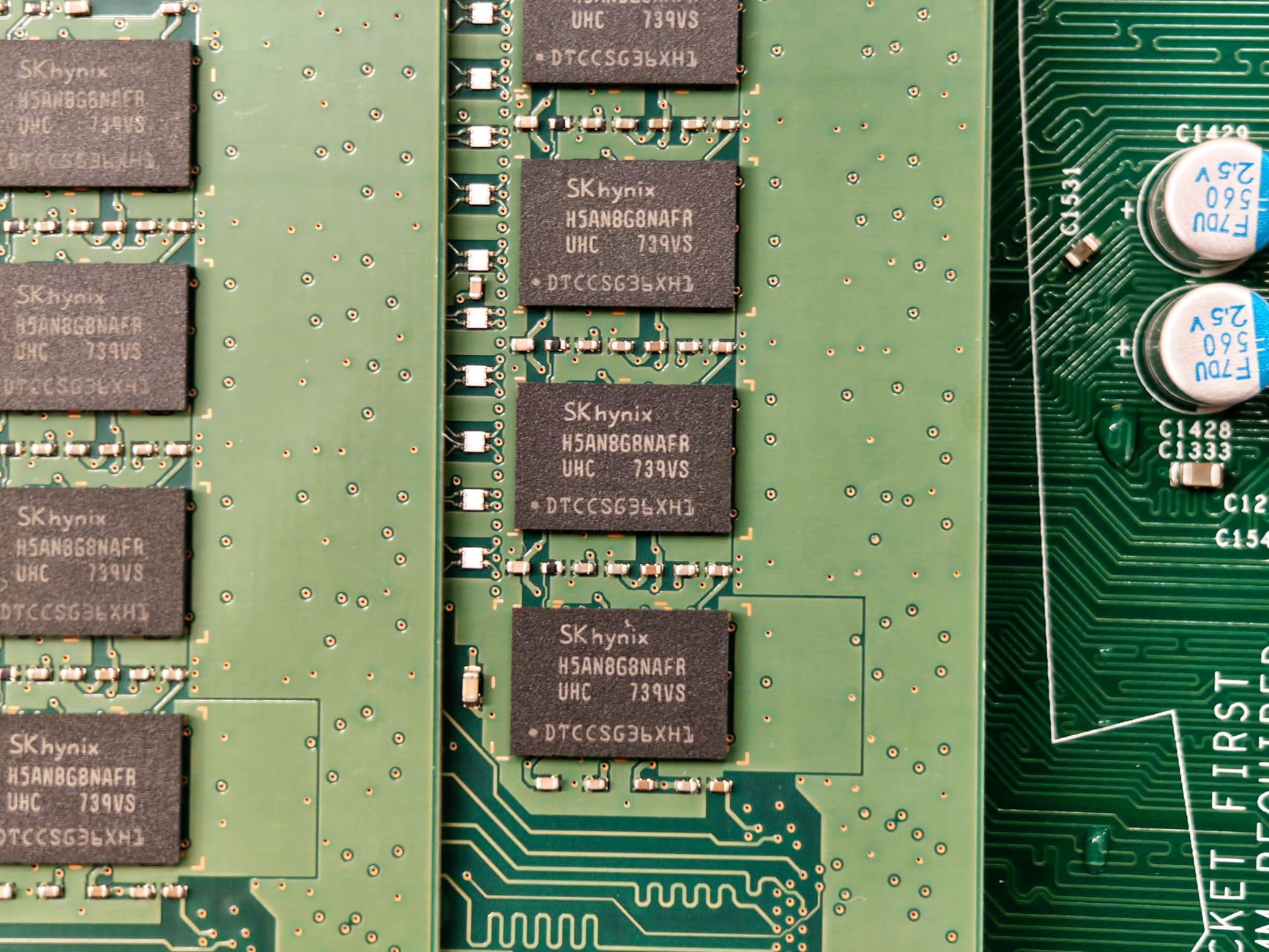

Hynix’s Billion Listing Tests the Memory Supercycle Outlook

The market is staring at SK Hynix’s upcoming $29 billion ADR listing as a pivotal barometer for how long the memory supercycle can endure. This is less a traditional IPO moment and more a liquidity and capital-formation move designed to broaden access to foreign investors. In an industry where pricing power has swung with demand from hyperscalers and data centers, the listing becomes a live stress test for whether the underlying cycle remains durable or hinges on cyclical momentum.

Viewed through the lens of the week’s earnings flow and price moves, the listing may reveal whether memory makers can translate pricing strength into sustainable profits. Traders are weighing how much of the recent upshift in DRAM and NAND pricing is structural versus a temporary bounce in a capex-heavy cycle. The outcome could shape sentiment across the sector for the next several quarters.

What the Market Is Watching This Week

Markets in Asia and Europe kick off a crucial stretch for memory shares as the ADR debut nears. The industry has seen scattered pockets of strength—from price hikes at key suppliers to resilient demand from data centers—but the pace and durability of those gains remain hotly debated.

Two signals are on the radar: SK Hynix’s ADR reception and a batch of earnings from peers that could tilt sentiment. If investors interpret the listing as a signal that global investors want in on memory exposure, the stock could gain momentum even as chipmakers face mixed macros and ongoing supply adjustments.

Additionally, memory pricing trends in Asia and the performance of large hyperscale buyers will influence expectations for 2026 and beyond. The sector has benefited from AI-driven compute needs, but any slowdown in AI deployment or a pullback in capex could test the durability of the current pricing regime.

Key Data Points Investors Are Reading

- ADR size: About $29 billion, signaling a major liquidity move rather than a traditional market debut.

- Micron Technology (MU) earnings context: Analysts are watching for a continuation of elevated server demand and margins that could set a floor for memory stocks.

- Samsung Electronics: Preliminary pricing trends for DRAM have shown some upward pressure in certain pockets, even as competition remains intense.

- Pricing and margins: Market chatter centers on whether the industry’s gross margins can stay firm as supply-demand cycles evolve and new capacity comes online.

- Demand signals: AI, cloud, and enterprise data workloads continue to power memory demand, but visibility remains uneven across regions.

Analysts Weigh In

Analysts warn that hynix’s billion listing puts the memory trade under a sharper lens than at any point in the current cycle. Market observers stress that the price path for DRAM and NAND in the next two quarters will be critical for interpreting this week’s events.

Analyst Mia Chen of MarketPulse said, "The memory cycle is being tested by this week’s developments, and the market will scrutinize whether demand proves persistent beyond the current upcycle."

Another strategist, Peter Ruiz at NorthBridge Partners, added, "Investors will be parsing capacity plans and price realization in tandem. If Hynix’s listing helps attract patient capital, it could reinforce the durability case for the memory supercycle; if not, we may see a reset in expectations."

Overall, analysts note that the hype around memory stocks has cooled from last year’s peak, but the sector remains a bellwether for tech capex and AI spending. The coming days will reveal whether the current strength is a sustainable shift or a pause before the next round of volatility.

The hynix’s billion listing puts the memory narrative to a real test

Beyond the immediate liquidity dynamics, the headline event highlights two central themes. First, the discipline of supply comes into sharper focus. Second, the durability of demand hinges on a broader connective thread between enterprise IT refresh cycles, AI-driven workloads, and consumer electronics needs. This week’s data points and company comments will influence how investors price risk in memory equities for the rest of 2026 and into 2027.

For some, the ADR listing represents a vote of confidence in the region’s ability to attract long-duration capital for high-beta, high-innovation sectors. For others, it is a reminder that the memory market remains highly sensitive to the ebb and flow of capital expenditure by major cloud providers and the rate at which new memory products capture price premium and efficiency gains.

What Could Tilt the Cycle Next

- Capex signaling from major memory players, including announcements around wafer capacity and fab utilization.

- Shifts in DRAM and NAND pricing power, particularly in pricing bands used by hyperscale customers.

- Macro stability in key markets, including enterprise demand for data center expansion and edge computing rollouts.

- Technological shifts, such as new memory tech that changes how memory is priced and deployed in AI workloads.

Bottom Line: A Week of Clarity for Memory Investors

The hynix’s billion listing puts a sensitive market on notice: the memory supercycle may survive the cyclical test, but it will require continued demand resilience and effective price discipline from producers. If investors read the ADR event as a sign that long-horizon money is embracing memory exposure, the sector could extend its recovery into late 2026. If the market interprets the listing as a one-time liquidity boost without lasting demand support, sentiment could snap back toward volatility as earnings from Samsung, Micron, and peers roll in later this week.

In an environment where AI demand and data center expansion still drive much of the narrative, memory stocks remain a macro-level proxy for tech capex and corporate IT budgets. The week ahead will likely settle how investors price that risk, and whether hynix’s billion listing puts the memory cycle on a more durable footing or simply prolongs the transition to a new phase of volatility.

Discussion