China’s Long‑Term Leverage Outruns Short‑Term Deals

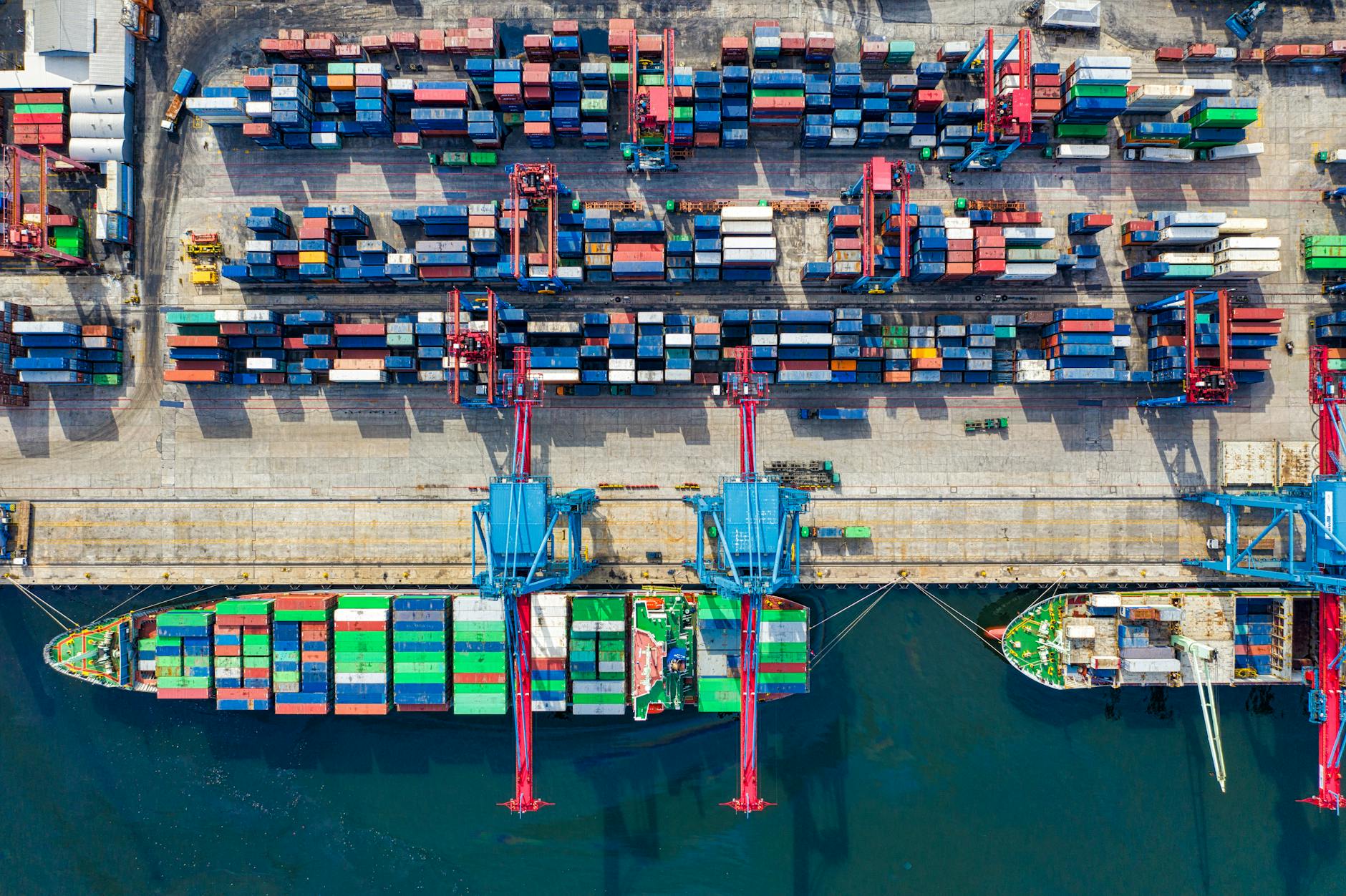

As global markets reassess supply chains in early 2026, Beijing’s stance remains anchored in a decades‑long trajectory rather than any one negotiation. Official data show China ran a trade surplus around $1.2 trillion in 2025 and is on pace to generate at least $1.25 trillion in export earnings in 2026. That scale anchors pricing power, supplier networks, and competitive quality that hard‑to‑match rivals struggle to replicate.

The practical takeaway for investors is simple: the country’s economic strength isn’t a hostage to a single round of talks. It’s a function of mass production capacity, integrated logistics, and a global footprint that continues to expand even as trade conversations unfold. In short, china doesn’t need trade to win; it already holds the strategic advantage that long‑term investors watch, even if headlines emphasize negotiation rooms and tariff timelines.

Why the Paris Talks Were Seen as Constructive—And Ultimately Limited

Recent diplomacy rounds in Paris produced what officials described as a calm atmosphere and a willingness to keep talking. Yet executives and analysts agree that any immediate breakthrough remains unlikely because each side seeks concessions the other side cannot concede without surrendering core interests. The effect on markets is a reality check: policy progress is incremental, while economic momentum persists on its own terms.

“China isn’t bargaining from weakness, but from decades of structural advantage,” says Maria Chen, a senior advisor at Global Strategy Partners. “That dynamic means outcomes in negotiations will be tactical at best, reframing reciprocity without compromising the core run of exports.”

What China’s Strength Means for Global Supply Chains

Global executives report ongoing import growth from China, not because they prefer it, but because viable substitutes remain scarce on a cost-competitiveness basis. For many product lines—electrical components, consumer electronics, and durable goods—Chinese suppliers still offer a combination of pace, price, and quality that is hard to beat.

- 2025 trade surplus: about $1.2 trillion

- Projected 2026 export earnings: at least $1.25 trillion

- 2026 export growth forecast: 10%–15%

- Share of global manufacturing capacity: broad cross‑sector dominance in cost and scale

Analysts emphasize that even with political frictions, the real risk for global buyers is disrupted timing rather than a wholesale re‑routing of production. “The structural network of factories, ports, and downstream suppliers has become a global circulatory system,” notes Alex Romero, chief strategist at NorthGate Asset Management. “That system is resilient in the face of policy noise.”

What This Means for Investors and Consumers in 2026

For U.S. households and investors, the message is nuanced. A steady, export‑led growth engine in China supports commodity demand and tech components that power many American products. At the same time, policymakers in the United States and Europe continue to recalibrate risk in the supply chain—diversifying sourcing, building stockpiles, and adjusting inventory strategies to mitigate potential shocks.

Market players are watching three threads: monetary conditions, demand in major export markets, and the policy tempo from Beijing. If the headline drama around trade talks continues, it could inject volatility. If momentum in China’s real economy remains resilient, portfolios could price in the consistency of export strength rather than the speed of any agreement.

How CEOs Are Reacting to a Trade Landscape That Isn’t Dependent on Deals

CEOs across manufacturing, consumer goods, and tech hardware are matrixing their supply chains around what remains a reliable anchor: China’s export engine. Many firms are integrating suppliers, moving some production closer to end markets, but they are not abandoning China as a core hub. The logic is clear: even in a more complex geopolitical climate, china doesn’t need trade to win because the economics of scale and logistics keep the country central to global manufacturing.

At a corporate level, the takeaway is practical: diversify where possible, maintain contingency plans for policy shifts, and monitor currency and energy price trends that could tilt costs. The base case remains that China’s export strength translates into pricing power for manufacturers and steady demand signals for investors.

Bottom Line: The Real Trade‑Off Is Policy Pace, Not Prosperity Pace

In March 2026, market participants should focus on how policy and geopolitics shape risk, not whether a deal will emerge this quarter. The enduring fact is that china doesn’t need trade to win, because the long‑run structural advantages underpin a robust export engine and a deep, efficient supply chain network. For investors, that means positioning for gradual growth, diversified sourcing, and careful attention to how tariff dynamics and currency moves interact with global demand.

Looking ahead, risk remains contained but real. If policy announcements align with the 2026 momentum in exports and industrial output, markets could reward exposure to Chinese manufacturing and consumer demand. If tensions spike, expect volatility in equities tied to global supply chains and in commodities tied to factory activity. Either way, the core leverage remains intact, and the question for investors is how to balance resilience with opportunity in a world where china doesn’t need trade to win.

Discussion